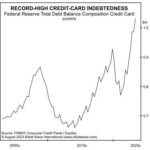

The following article by Elliott Wave International looks at the possible impact of the building debt crisis. We’ve all heard about the massive problem of College debt created by the easy-money policies of the government. But today we are looking at the impact of the massive credit card debt.

Is a Pension Fund Crisis Next?

May 12, 2023 by Leave a Comment

Many public pensions suffer from funding shortfalls. In other words, they don’t have nearly enough money to meet their obligations. More than that, investments are being made in potentially financially dangerous assets to boost returns, such as private equity.

Silicon Valley Bank, Silvergate and “The Everything Bust”

March 22, 2023 by Leave a Comment

the FED’s raising interest rates has resulted in an “inverted yield curve” (i.e. short rates are higher than long interest rates) which puts extreme stress on banks and has resulted in some recent bank failures. In this article, the editors of Elliott Wave International look at the banking situation. ~Tim McMahon, editor

Banks Are Becoming More Cautious About Lending

November 17, 2022 by Leave a Comment

With the FED tightening and raising rates, member banks are feeling the pinch and are being forced to adjust their lending practices. The COVID panic of 2020 and 2021 pushed mortgage rates to record lows below 3%. But with the FED’s money pumping during the same period, inflation soared to over 8%. Initially, the FED felt the inflation surge was “transitory” and was the result of supply shortages due to limited production during the pandemic. So, they refused to change their easy money stance. However, as inflation continued to surge, the FED eventually decided that it had to act.

So the FED began tightening (i.e., reducing FED assets), and raising FED funds rates. As we can see in the chart below, the FED funds rate was virtually zero at the beginning of 2022, and by October, it had shot up to 3.08%.

What the “Housing Busts” Indicator Is Saying Now

July 28, 2022 by Leave a Comment

The housing market tends to go the way of the stock market, and nearly everyone knows that the stock market has been sliding… Homes sales have already begun to decline:

U.S. existing home sales fall for third straight month; house prices at record high (Reuters, May 19)

Sales of existing homes fell in May, and more declines are expected (CNBC, June 21)

Sales of luxury homes in some areas have dropped significantly. As examples, in Nassau County, NY, Oakland, CA, Dallas, TX, Austin, TX and West Palm Beach, FL, annual drops in the rate of upper-end home sales for the three months ended April 30 stretched from 32.8% to 45.3%.

Why Investors are Consistently Fooled by the Stock Market

May 19, 2022 by Leave a Comment

Stock market observers are trying to “make sense” of the wild price moves, which have mainly been to the downside.

As a May 12 CNBC headline says:

Traders search for answers as relentless selling on Wall Street looks to be detached from reality

Many market participants believe the “reality” of economic statistics, earnings and other factors external to the market govern the market’s trend.

However, that’s a fallacy.

Let’s get insights from a classic Elliott Wave Theorist, a monthly publication which provides analysis of financial markets and social trends:

Are Disease Outbreaks Market Indicators?

November 20, 2021 by Leave a Comment

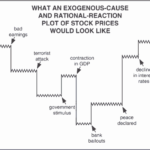

Waves of social mood fluctuate in accordance with the Wave Principle and determine prices in financial markets. Moreover, these same waves regulate the tenor and character of social attitudes and actions. The key point is that social mood is the cause. It is endogenous. Prices in financial markets and events in society are the effects. They are exogenous.

However, most people believe the opposite is true.

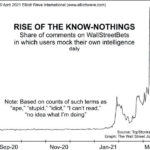

Rise of the “Know Nothings”

May 1, 2021 by Leave a Comment

With the longest “Bull market” in history in full swing young investors are flocking to the market with no experience of ever having seen a full-fledged crash only “corrections” that are quickly reversed into higher and higher valuations. Twenty-somethings were still in elementary school in 2008 so it is a distant memory… let alone 2002-3 or 1989. With no experience in dealing with a crash, they are plunging into the market at record levels.

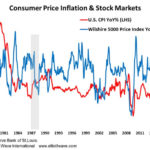

Should Stock Markets Fear Inflation or Deflation?

March 31, 2021 by Leave a Comment

You can’t go ten minutes on financial media these days without coming across a reference to inflation. That is, consumer price inflation to be more exact — the measurement of changes in the prices of consumer goods and services that the entire world has been hoodwinked by central banks into thinking is the definition of inflation. The proper definition of inflation is the expansion of money and credit in an economy. On that definition, most major economies have been experiencing high inflation for decades.

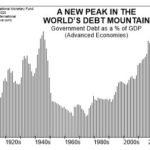

A Global “Debt Mountain”: Beware of This “New Peak”

March 18, 2021 by Leave a Comment

Most people going about their daily business probably never give a moment’s thought to global debt. But, in EWI’s view, the topic deserves serious attention. You only have to think back to the 2007-2009 subprime mortgage meltdown to know why. Of course, subprime mortgages are a form of debt, and when many of these loans turned sour, the entire global financial system teetered on the brink of collapse. But, why were so many of these bad loans made in the first place? It boils down to one word: confidence … confidence that the loans would be repaid, confidence that the stock market would continue to rally, confidence in the economy, and confidence in the future, in general.