Regular readers know our approach involves meticulously paying attention to known information about the markets and making allocation adjustments when conditions change. Small caps provide a recent example of how this approach can be helpful to investors and traders.

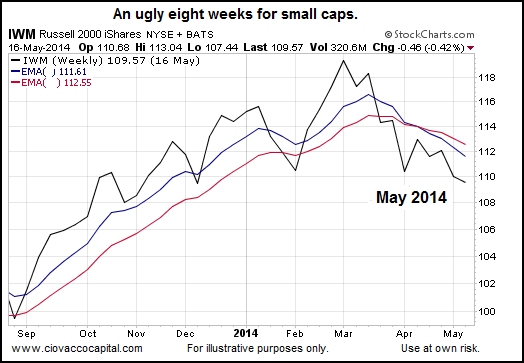

May 2014: Small Caps Were Concerning

During the first three weeks of May, it was easy to find “small caps are waving yellow flags” articles or tweets similar to the blurb below published on Nasdaq.com:

During the first three weeks of May, it was easy to find “small caps are waving yellow flags” articles or tweets similar to the blurb below published on Nasdaq.com:

On the surface, this may seem like a somewhat benign decline of 9% from the 2014 highs in IWM. However, there is some legitimate concern mounting that small-cap stocks may become a leading indicator of weakness that will spill over into the rest of the market. It would not be surprising to see this index lead a correction lower after being one of the strongest segments during this bull market.

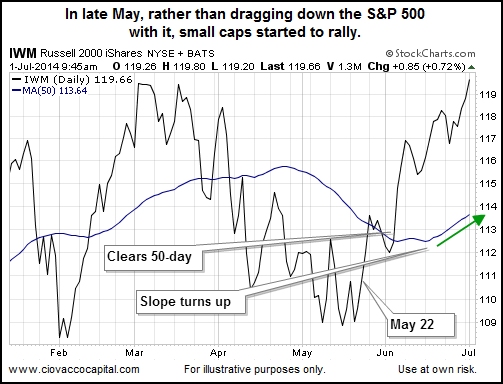

Late May: Don’t Assume Small Caps Can’t Turn It Around

One of the strengths of always maintaining a flexible investment stance is it allows you to consider both bearish and bullish outcomes. Contrast that with looking at the May 2014 weakness in small caps with a bearish bias for stocks. If you have a bearish bias, you know what is going to happen: (a) small caps will continue to drop, and (b) it is only a matter of time before the S&P 500 follows. On May 21, we penned the following:

It is not safe to assume that 2014 cracks in small caps can only widen.

Small caps could rally in 2014 as they did in 2013.

July 2014: Small Caps Turn, Stocks Rally Further

On May 14, a week before small caps turned, we discussed the concept of “forecasting brings investment bias”. The passage below is relevant to today’s small cap analysis:

When we talk about ego in an investment context, we are talking about the intense human desire for our opinions and stance to be confirmed by the markets and other human beings. In short, we all want to be right. If we are to become more relaxed and better investors, we need to have a healthy and sound understanding of what “being right” means. Experienced investors who got tired of common investment missteps started a process of ongoing improvement by seriously contemplating this question: What is more important to me: (A) protecting and growing my capital, or (B) protecting my desire to “be right”?

Bias and ego bring filters into the investment process, which make it much harder to identify important shifts in the market’s tolerance for risk. For example, if you were confident small caps would correct further and eventually the stock market would follow, it was difficult to react to the observable improvement in small caps that began on May 23.

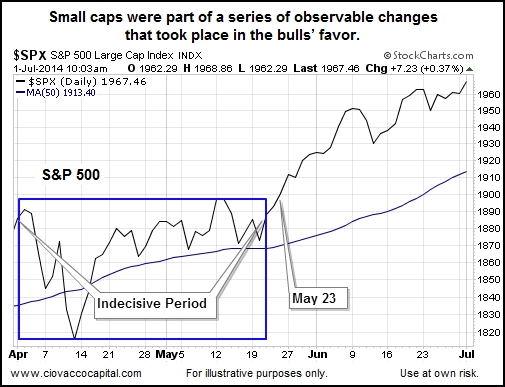

What Happened Next?

Since small caps started to signal a renewed desire to own growth-oriented assets on May 23, the S&P 500 has tacked on 73 points.

Does Flexibility Help?

Yes. We made the comments below after the market closed on May 23:

As of Friday’s close, the weight of the evidence still sides with the bulls. Our market model uses numerous inputs to assist us with a “monitor and adjust” approach, which is quite a bit different than an “anticipate and hope” strategy. The observable improvement that occurred over the last five sessions enabled the model to recommend a slight increase to the growth side of our portfolios. Therefore, Friday we added to our stock holdings and reduced our money market balances.

There are two main takeaways from the May 23 comments above: (a) even on May 23 the “weight of the evidence” sided with the bulls, which speaks to investing based on hard data rather than fear of what may happen, and (b) flexibility allowed for an increase in the allocation to the growth side of the portfolio based on “observable improvement”.

China, Japan Help Global Stocks

The S&P futures were green early Tuesday morning based in part on good economic news from foreign lands. From Reuters:

China’s final reading of the HSBC/Markit purchasing managers’ index (PMI) for June rose to 50.7 from May’s 49.4, edging past the 50-point level that separates growth in activity from contraction for the first time since December. Manufacturing in Japan, the world’s third-biggest economy, also gained pace in June, fueled by improving demand at home, but euro zone growth faltered as Germany, the region’s top economy, slowed.

Big Deals Helping Bulls

If you follow merger and acquisition chatter, you know “big things have been brewing” for years. Well, the talk is being converted into big deals in 2014. From Bloomberg:

After like four years of “not a lot of deals but the backlog is strong,” the backlog has arrived. Highlights: $1.77 trillion of mergers and acquisitions in the first half of 2014, the most since 2007. It’s driven by big deals; the number of deals announced in the first half is the lowest since 2005.

Investment Implications – Bulls In Control Until Something Changes

We came into the week with a heavy allocation to stocks (SPY), and leading sectors such as technology (XLK). While we still hold a complimentary and off-setting exposure to bonds (TLT), that side of the portfolio has been reduced as the growth side has been increased over the past eight weeks. How long will we stay with stocks? …until an observable shift occurs in the market’s tolerance for risk. The video 2008: Was There Anything Investors Could Have Done? provides a detailed example of what a deteriorating risk-reward profile looks like.

Copyright © 2014 Ciovacco Capital Management, LLC. All Rights Reserved. Chris Ciovacco is the Chief Investment Officer for Ciovacco Capital Management, LLC (CCM). Reprinted by permission. This article originally appeared here and was reprinted by permission.

[…] Adjusting Your Investments […]