By Jeff Clark, Senior Precious Metals Analyst

For many primary gold producers, Q2-2013 was a breathtakingly bad quarter. It wasn’t so much the massive drop in earnings many reported—those had been, for the most part, expected—but the so-called “impairment charges” announced.

(Impairment is the opposite of appreciation, that is, the reduction in quality, strength, amount, or value of an asset. “Impairment charges” means that a company reduces or “writes down” the value of the assets on its books.)

The gold price averaged $1,630.45 in Q1 this year, falling to $1,413.64 in Q2. The downturn squeezed profit margins, obviously, but it did the greatest damage to the value of many company assets that are based on gold.

But what will happen to those same assets if the gold price is on the rise again? What does it mean for us as investors? I’ll answer these and more questions below.

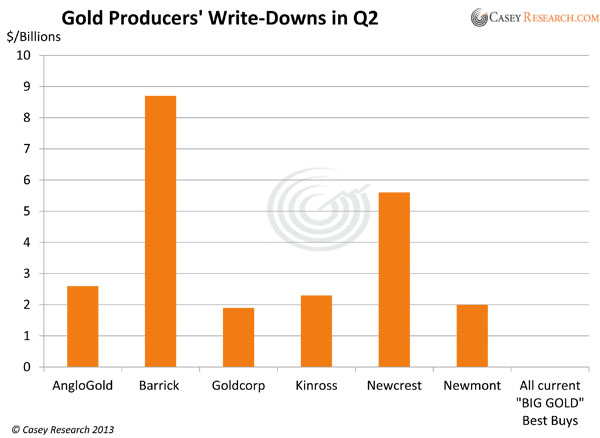

First, here’s a look at the amount of write-downs the six largest primary gold producers announced last quarter.

The explanation the companies gave for these impairment charges was essentially the same in every case: short- and long-term gold price assumptions that hadn’t panned out. Total losses for just these six producers were $23.1 billion. That’s a lot of dough to send to money heaven, for a relatively small industry. Food for thought.

Here’s what you need to know as an investor in this sector.

How does an impairment charge occur?

In public companies, management must report a reasonable value of company assets to shareholders and the public. If labor or other production costs rise, they may have to reassess the value of the company’s assets.

In this case, the price of gold—the product many of our companies sell—dropped 13.3% in just three months, and did not seem likely to rebound immediately. Of course, that changed the amount of earnings investors could expect from a gold mine. Companies had to revise the net present value of projects in development, or the book value of mines in production, with the new reality for gold in mind.

But isn’t gold always fluctuating?

Yes, but the accounting is (meant to be) conservative. The last thing any management team wants is to be forced to tell the market that its projections were wrong and profits are much less than anticipated—or worse, nonexistent. Shares would plummet, management would have a major credibility problem (perhaps a legal one as well), and heads would roll.

What companies are supposed to do is look out to the horizon and project the lowest (safest) reasonable price assumptions they can, for the foreseeable future. Some are better at it than others, and some mining companies that used too aggressive price assumptions in their economic studies ended up, in the worst-case scenario, abandoning projects.

On the other hand, it’s just as bad if management overreacts to temporary price swings. A long-term view should position the company so that short-term price fluctuations—up or down—don’t seriously affect the value of a project. In other words, they try to allow for normal volatility.

How do they know how much to write down?

If management believes prices have changed so much that it affects the value of company assets, they conduct a formal “impairment test.” If an asset doesn’t pass, the amount of the charge is the difference between the old book value and the recoverable value, or the fair market value for the asset at that point in time.

So the companies that had no write-downs are more conservative?

The better ones are—others may simply be refusing to face the fact that gold is still below the three-year trailing average that was typically used as a price assumption. A cautious gold company that, say, valued an asset assuming $1,100 gold should not have needed to file an impairment charge last quarter (all other things being equal). Gold has averaged $1,303.33 so far in Q3, well above the price that returns were projected from.

For example, major gold producers Yamana and Agnico-Eagle were able to avoid impairment charges last quarter. As the chart above shows, all producers currently rated a Best Buy in BIG GOLD had no write-downs. As an owner of these stocks, I was glad to see this. It also confirmed that we’ve selected management teams that are both shrewd and conservative.

What happens when a write-down turns into a write-off?

While a write-down is a mere reduction in value, a write-off eliminates that value altogether. For some companies, a project may not just be less profitable, but completely uneconomic at lower gold prices. If total production costs were $1,400 per ounce, for example, that project would have zero value at today’s prices. This sometimes happens with low-grade mines.

This is the reason so many projects have been suspended or moved to the back burner over the last few months—and rightly so. We believe gold will move back up and hit new highs, but that’s not the conservative stance corporate management should take, especially when deciding to invest billions of dollars building a large new mine.

These projects can be revived when gold prices go up again, but they will need to be reevaluated when things change, particularly regulatory and cost factors.

What happens if the price of gold goes back up?

In the past, companies were stuck. Until very recently, impairment charges were a one-way street. Once you took the charge, you lived with it. But there are some new rules that permit the accounting to go both ways.

These new international rules were instituted in 2011 and haven’t yet been tested for higher values in the resource sector. But if the gold price recovers and there are strong reasons to believe it will stay there (something we see as highly likely), it’s possible we could see some of these impairments reversed. That’s what you might call a “write-up.”

Here’s an interesting consequence for speculators: Once a company has written down an asset, that loss no longer trickles down to the bottom line in the form of depreciation expense.

Suppose you have a mine written down to zero, because operations provide effectively zero return at lower prices, but the company keeps mining because management believes prices will go up, and mine closure would be both expensive and hard to reverse. Then prices do rise, and the mine starts making money hand over fist, with no depreciation to impact net income.

That’s why it’s so important to separate still-viable assets that are written down from those that really were based on foolish assumptions and are never likely to be profitable.

Should I sell my companies that reported write-downs?

Not necessarily. As I said above, it’s not the end of the world if a company is forced to write down an asset. The question is whether the company will be able to survive the current price environment and have a shot at better profits in the future.

To know when to hold, fold, or be bold, sign up for a three-month trial to BIG GOLD, with full money-back guarantee.

Even with gold’s steep correction, a handful of Best Buy companies in our portfolio had very impressive Q2 results—but despite their above-average performance, they are still severely undervalued. I expect them to do so well that I’ve added some of them to my own mother’s portfolio (and she only allows for the safest bets).

Find out which stocks Doug Casey and his team see as the top performers in the recovery. You have nothing to lose—click here to try BIG GOLD for just $129 per year. If you don’t absolutely love it, cancel within the first three months for a full refund.

Speak Your Mind